For working professionals

For fresh graduates

- Study abroad

More

- Post Graduate Certificate in Data Science & AI (Executive)

- Gen AI Foundations Certificate Program from Microsoft

- Gen AI Mastery Certificate for Data Analysis

- Gen AI Mastery Certificate for Software Development

- Gen AI Mastery Certificate for Managerial Excellence

- Gen AI Mastery Certificate for Content Creation

- Post Graduate Certificate in Product Management from Duke CE

- Human Resource Analytics Course from IIM-K

- Global Master Certificate in Integrated Supply Chain Management

- Gen AI Foundations Certificate Program from Microsoft

- CSM® Certification Training

- CSPO® Certification Training

- PMP® Certification Training

- SAFe® 6.0 Product Owner Product Manager (POPM) Certification

- Post Graduate Certificate in Product Management from Duke CE

- Professional Certificate Program in Cloud Computing and DevOps

- Python Programming Course

- Executive Post Graduate Programme in Software Dev. - Full Stack

- AWS Solutions Architect Training

- AWS Cloud Practitioner Essentials

- AWS Technical Essentials

- The U & AI GenAI Certificate Program from Microsoft

Economics Masterclass Online Courses

The study of economics can be applied in several sectors of the economy like business, health care, finance, engineering, government, and even households. Read more below

20(1)-70997669bd1a4ba2b565901e0eae2fa5%20(1)-de9c82be352d44bcb6a48fecf60b4465.jpeg&w=3840&q=75)

Economics Masterclass Course Overview

The subject area of economics analyses the behaviour and interactions of people while allocating scarce resources. It ensures the responsible and optimum utilisation of limited resources to maintain an ideal balance in the economy. It keeps a close check on the functions of the entire economy as well.

To properly manage every sector of the economy, there are two subsections of economics, Microeconomics and Macroeconomics. Besides these, other broad distinctions of economics are positive economics (what is), normative economics (what ought to be), economic theory and applied economics, rational economics, and behavioural economics.

The study of economics can be applied in several sectors of the economy like business, health care, finance, engineering, government, and even households.

Economics is the study of the responsible allocation of resources by individuals and higher authorities for future production, distribution, and consumption, both at the micro and macro-level. It primarily focuses on efficiency during production and exchange.

When a person has unlimited wants but limited resources, there must be a definite plan for optimum utilisation of available resources. Here, the economists analyse the decisions made by an individual, business, or economy as a whole and find ways to accommodate unlimited wants with limited resources.

The world of economics revolves around scarcity and choice. Scarcity means when a human's desire or need for goods or services exceeds the actual amount of resources available. On the other hand, their choices in distributing those scarce resources to achieve maximum satisfaction are the essence of economics. Some tools and indicators are used to analyse people's decision-making about scarce resources. The study of economics can be used in almost every industry to balance available resources and the need for them.

Economics is also termed social science, which focuses on the study of production, distribution, industries, consumption of goods and services, government policies, and many other things. Apart from this, Economics has various other natures, and the implementation of it through those views are different from one another.

Economics as a science is associated with the cause and effect relationship, and it also analyses different economic factors before jumping to a conclusion. Here, some other elements of science are added, like statistics and mathematics, to comprehend the relationship between price, supply, demand, and several other elements.

Under this, there are two types of economics.

- Positive Economics- It evaluates the relationship between two variable factors but does not make any judgment. It just reflects the actual condition and deals with the facts related to the economy.

- Negative Economics- Economics transfer value judgment, i.e., ‘what ought to be.’ This form of normative science is used in policies that are required to achieve these policy goals.

Economics as arts approaches problems practically and provides a unique and creative solution to them. It has several sections to take charge of, like the department of delivery, finance, creation, and consumption. Apart from these, it also takes care of implementing standard rules and regulations that are essential to solving complex societal issues.

Therefore, economics can be recognised as science as well as art. Science shows the methodologies involved in economics, whereas art reflects its application both in professional and practical aspects of the economic problem.

The field of economics is wide, and to study every aspect thoroughly, one must need to break it down into several parts. This whole subject is broadly divided into three main parts, Microeconomics, Macroeconomics, and Econometrics.

Each of these types has its way of observing and handling the stability of human wants and needs. From hereon, we will get deep into these sections of economics separately to understand the essence and importance of economics in an economy.

Microeconomics

This branch of economics deals with the choices an individual, household, or firm makes regarding the allocation of resources. Microeconomics studies the various factors involved in selecting scarce resources and the effect of those decisions on the economy. It scrutinises the factors influencing people while choosing a resource that meets their needs. Subsequently, it also inspects the effect those decisions have caused in the market or economy by deflecting the price, supply, and demand.

In a nutshell, microeconomics deals with the supply and demand of various markets. It analyses and demonstrates the relationship households and businesses share and their interaction's impact. Several economic activities go between a household and business, like purchasing household goods and services, selling own resources by individuals, and many others.

The primary focus of microeconomics is on the variables that affect individual economic decisions, their impact on each decision-maker, and how demand and prices are established in specific markets. It analyses the market process that eventually sets the prices for goods and services in the market for all. In brief, it demonstrates the circumstances under which open markets finally result in favourable distributions. Moreover, it also examines market failure, i.e., when the market is unable to deliver useful outcomes.

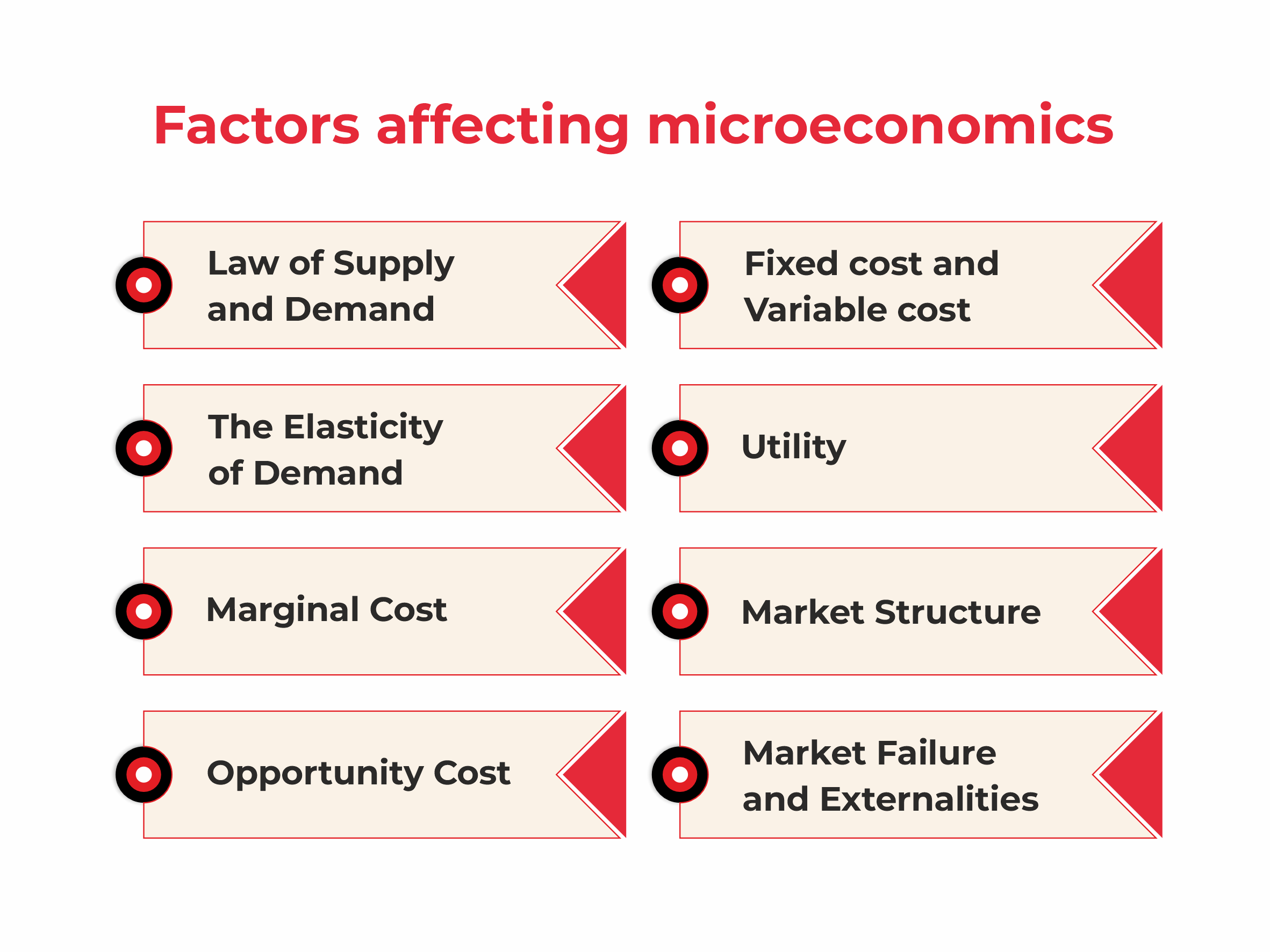

The study of microeconomics considers various factors while assessing the behaviour of individuals and firms. Some of the factors are mentioned below;

- Law of Supply and Demand

- Fixed cost and Variable cost

- The Elasticity of Demand

- Utility

- Marginal Cost

- Market Structure

- Opportunity Cost

- Market Failure and Externalities

Macroeconomics

After observing the changes on a micro level, this branch of economics deals with the nation's economy. It focuses on the changes in the economic output, interest on foreign exchange rates, GDP, changes in employment, and inflation, as these essentials determine sound growth of society/economy.

Macroeconomics deals with the entire economy's performance, structure, and behaviour while analysing. As it considers the whole economy, the working areas in macroeconomics are divided into two broad parts: long-term economic growth and the short-term business cycle.

Examining every sector/industry of the economy and its correlation is crucial to understanding the nation’s economy. By making necessary observations, the economists develop models that explain the changes in the economy due to variables like GDP and inflation. These models and forecasts thus, make a path for the government to work on. From hereon, the government entities use these assessments to construct and evaluate new economic, monetary, and fiscal policies that can help develop the economy.

Apart from the government, businesses use these predictions to set strategies in domestic and global markets; the investors also make the most out of it by planning the movements in various asset classes. This gives the investors and businesses a thorough understanding of the effects of new economic trends and policies on their industries.

The entire process must be executed with mindfulness as the study of macroeconomics works on an enormous scale.

Econometrics

This interesting branch of economics uses statistical and mathematical models to develop theories and predict future trends from historical data. In simple terms, it turns theoretical economic models into useful tools for economic policymaking. The methods used in econometrics rely on the statistical conclusion to analyse economic theories with the help of tools like probability, frequency distribution, correlation analysis, and many others.

In basic terms, econometrics makes things more practical and calculative in nature. It transforms qualitative statements into quantitative statements and theoretical models into something that can be calculated or estimated. It is thus a practical approach in the field of economics.

There are several sections of economics where econometric methods are used to gain effective results, such as;

- Macroeconomics

- Microeconomics

- Finance

- Labour Economics

- Economic Policy

One of the basic tools for econometrics is the multiple linear regression model that models a relationship between a scalar response and more than one explanatory variable. The professionals in this field or the econometricians try to find estimators that everyone can rely on, and they should also possess statistical properties like unbiasedness, consistency, and efficiency.

Though it is a science, econometrics can also be considered an art that demands considerable judgment and can eventually obtain useful estimates for policymaking.

While understanding economics, we must know the basic economic terms and concepts used in this world. Most of these terms are usual and are part of our daily life but generally, we don’t look at them through the lens of economics. Let’s get some insights on these terms.

1. Supply and Demand

Supply and demand are generic processes that are easy to spot around us. To understand these two more clearly, we must take an example. For instance, a person goes out to buy vegetables, and there are different prices for every product because of its multiple meditators. But when the buyer and sellers finally meet at a particular price, then that is what we call the state of supply and demand, where demand meets the supply.

2. Value for Money/ Costs and Benefits

In simple terms, value for money defines the utility derived after spending any amount to purchase any service or product. The value that you are deriving after the expense that you have made. This can easily justify the pricing of a commodity; there is a specific price for every good and service, which is given considering the amount of utility it will provide. Thus, the basic rule is to spend money on goods and services according to their utility.

3. Scarcity

Scarcity is a common term that we understand, but in economics, it is related to the limited/scarce resources available to meet our unlimited wants. Perceiving the real-world conditions, scarcity is heavily taken into consideration to make economic decisions. That includes their choice of allocation of available resources in an optimum way that satisfies their maximum wants. Scarcity of something makes the person responsible while using it.

4. Opportunity Cost

Our world offers multiple things. If we tend to buy one, there are plenty of options to choose from. Hence, you will always lose something or other while choosing the best for yourself. So, the item that you did not choose, you tend to pay an opportunity cost for that. For example, if you decide to spend Rs. 3000 on a pair of jeans rather than getting the required set of books, the opportunity cost would be the money you could’ve spent on the books and several other things.

5. Purchasing Power

It simply means the ability of a person to buy any product or service. Purchasing power is defined by the amount of money one has. It can also be termed as the currency's value expressed through the number of goods and services that one unit of that money can buy. There can be a serious jolt in the purchasing power of someone due to inflation. This happens when the income remains the same, but commodities' price rises.

Apart from all the concepts mentioned above in economics, there are some basic terms that you should know about.

- Commodity- These are the raw materials that are purchased in huge quantities for the process of production

- Equity- It can be described as the ownership of an asset.

- Elasticity- This reflects the amount of change in an economic variable in response to another, like when the demand increases when the prices are low and vice versa.

- Liquidity- The ease with which an asset gets converted into cash without changing the market price.

- Leverage- The technique of purchasing stuff with borrowed money in the hopes that future profits will be much more than the cost of borrowing.

- GDP- It can be defined as the total value of goods and services produced in a country in a specific timeframe.

- GNP- It is slightly different from the GDP as it calculates the production of goods and services by the citizens of the nation from wherever they are within a specific financial year.

- CPI- It measures the changes in the prices of goods and services acquired by individuals to satisfy their wants. When CPI increases, it indicates an increase in inflation.

- Inflation- It reflects the rate of increase in prices of goods and services over some time. It translates as an increase in the cost of living.

- Economic Depression- It is that period for a country’s economy when it suffers from a long-term downturn and a state of financial turmoil

Best Management Courses

Programs from Top Universities

Our management certification courses cover a wide array of management principles and practices, making them some of the best management courses in India. Whether you are a new manager or an experienced professional looking to update your skills, our management degree courses offer valuable insights

Management (0)

Loading...

upGrad Learner Support

Talk to our experts. We are available 7 days a week, 9 AM to 12 AM (midnight)

Indian Nationals

1800 210 2020

Foreign Nationals

+918068792934

Disclaimer

1.The above statistics depend on various factors and individual results may vary. Past performance is no guarantee of future results.

2.The student assumes full responsibility for all expenses associated with visas, travel, & related costs. upGrad does not provide any a.