All courses

Agentic AI

Agentic AI

IIIT Bangalore

Executive Programme in Generative AI for LeadersArtificial Intelligence

Degree / Exec. PG

IIIT Bangalore

Executive Diploma in Machine Learning and AI

OPJ Global University

Master’s Degree in Artificial Intelligence and Data Science

Liverpool John Moores University

Master of Science in Machine Learning & AI

Golden Gate University

DBA in Emerging Technologies with Concentration in Generative AIExecutive Certificate

IIITB & IIM, Udaipur

Chief Technology Officer & AI Leadership ProgrammeIIIT Bangalore

Executive Programme in Generative AI for Leaders

upGrad | Microsoft

Gen AI Mastery Certificate for Software DevelopmentupGrad | Microsoft

Gen AI Mastery Certificate for Managerial ExcellenceOffline Bootcamps

upGrad

Data Science and AI-MLDoctorate

For All Domains

IIITB & IIM, Udaipur

Chief Technology Officer & AI Leadership Programme

Swiss School of Business and Management

Global Doctor of Business Administration from SSBM

Edgewood University

Doctorate in Business Administration by Edgewood UniversityGolden Gate University

Doctor of Business Administration From Golden Gate University

Rushford Business School

Doctor of Business Administration from Rushford Business School, SwitzerlandGolden Gate University

Master + Doctor of Business Administration (MBA+DBA)-d9bdeff6165f4eb1ba2adcebde78e961.svg)

University of Waterloo

Chief Technology and AI Officer ProgramLeadership / AI

Golden Gate University

DBA in Emerging Technologies with Concentration in Generative AIMachine Learning

Machine Learning

Data Science

Degree / Exec. PG

O.P Jindal Global University

Master’s Degree in Artificial Intelligence and Data ScienceIIIT Bangalore

Executive Diploma in Data Science & AILiverpool John Moores University

Master of Science in Data ScienceExecutive Certificate

upGrad | Microsoft

Gen AI Foundations Certificate Program from MicrosoftupGrad | Microsoft

Gen AI Mastery Certificate for Data AnalysisupGrad | Microsoft

Gen AI Mastery Certificate for Software DevelopmentupGrad | Microsoft

Gen AI Mastery Certificate for Managerial ExcellenceupGrad | Microsoft

Gen AI Mastery Certificate for Content CreationOffline Bootcamps

upGrad

Data Science and AI-MLupGrad

Data AnalyticsMBA

Masters

Paris School of Business

Master of Science in Business Management and TechnologyO.P.Jindal Global University

MBA (with Career Acceleration Program by upGrad)Edgewood University

MBA from Edgewood UniversityO.P.Jindal Global University

MBA from O.P.Jindal Global UniversityGolden Gate University

Master + Doctor of Business Administration (MBA+DBA)Executive Certificate

IMT, Ghaziabad

Advanced General Management ProgramMarketing

Executive Certificate

Offline Bootcamps

upGrad

Digital MarketingManagement

Degree

O.P Jindal Global University

MSc in International Accounting & Finance (ACCA integrated)

Golden Gate University

Master of Arts in Industrial-Organizational PsychologyExecutive Certificate

IIIT-B & IIM, Udaipur

Chief Technology Officer & AI Leadership ProgrammeIIIT-B & IIM, Udaipur

Chief Data and AI Officer Programme

IIM Kozhikode

Human Resource Analytics Course from IIM-KupGrad | Microsoft

Gen AI Foundations Certificate Program from MicrosoftEducation

Education

Northeastern University

Master of Education (M.Ed.) from Northeastern UniversityEdgewood University

Doctor of Education (Ed.D.)Edgewood University

Master of Education (M.Ed.) from Edgewood UniversityCertifications

Project Management

Certification

Knowledgehut

Leadership And Communications In ProjectsKnowledgehut

Microsoft Project 2007/2010-ae8d039bbd2a41318308f8d26b52ac8f.svg)

Knowledgehut

Financial Management For Project ManagersKnowledgehut

Fundamentals of Earned Value Management (EVM)Knowledgehut

Fundamentals of Portfolio ManagementKnowledgehut

Fundamentals of Program Management-35c169da468a4cc481c6a8505a74826d.webp&w=128&q=75)

Knowledgehut

CAPM® CertificationsKnowledgehut

Microsoft® Project 2016Certifications & Trainings

-7f4b4f34e09d42bfa73b58f4a230cffa.webp&w=128&q=75)

Knowledgehut

PMP® CertificationKnowledgehut

PMI-RMP® CertificationKnowledgehut

PMP Renewal Learning PathKnowledgehut

Oracle Primavera P6 V18.8Knowledgehut

Microsoft® Project 2013Knowledgehut

PfMP® Certification CourseKnowledgehut

Project Planning and MonitoringPrince2 Certifications

Knowledgehut

PRINCE2® FoundationKnowledgehut

PRINCE2® PractitionerKnowledgehut

PRINCE2 Agile Foundation and PractitionerKnowledgehut

PRINCE2 Agile® Foundation CertificationKnowledgehut

PRINCE2 Agile® Practitioner CertificationManagement Certifications

Knowledgehut

Project Management Masters Certification ProgramKnowledgehut

Change ManagementKnowledgehut

Project Management TechniquesKnowledgehut

Product Management Certification ProgramKnowledgehut

Project Risk Management- Study abroad

- Offline centres

- uGSOT - B.Tech

More

%20(2)-db0b6f38da9c485faf76e366793c9b9e.webp&w=128&q=75)

Financial Analysis Courses Online

Financial Analysis Courses teach you how to evaluate financial statements, assess company performance, and make informed investment decisions. Learn ratio analysis, forecasting, valuation techniques, and Excel-based modeling to build strong analytical skills for finance and business roles.

20(1)-70997669bd1a4ba2b565901e0eae2fa5%20(1)-de9c82be352d44bcb6a48fecf60b4465.jpeg&w=3840&q=75)

Financial Analysis Course Overview

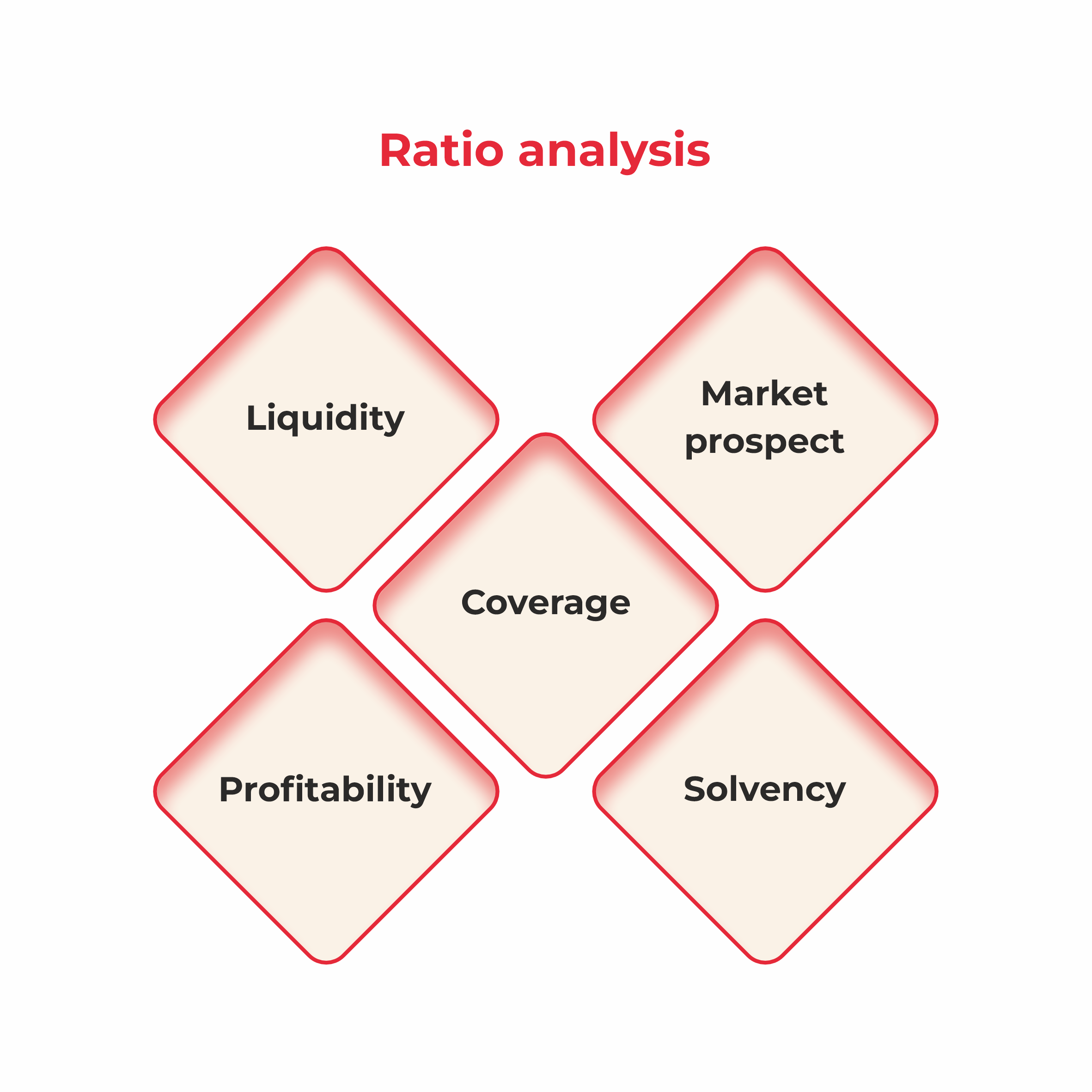

The financial analysis evaluates a company’s historical and present data to derive insightful information about the business's financial health and to forecast the same for the future. It helps the company in a variety of ways, from developing to engaging in strategic planning to prevent future hurdles.

The financial analysis process starts by collecting the data to make the financial statement and then examining them using several analytical tools and techniques. The financial statements provide knowledge of a company’s financial health and performance. So, it is of utmost priority for any investors, creditors, or businesses to analyse the company's financial statements per their needs.

There are various users of financial analysis like businesses, shareholders or investors, creditors, and even the government. However, their purpose in analysing a company’s financial statement differs.

One can study the whole business and get most of its information by analysing its financial statement. These reports carry information about every business transaction and reflect its performance, stability, and position in the market over a specific period.

Financial Analysis is an important tool of a business and can be used by the company to excel itself.

Financial Analysis Courses Instructors

Learn From The Best

Learn from industry experts in Financial Analysis Courses and gain real-world insights to master valuation, forecasting, and smart financial decision-making.

12

Instructors

Success Stories

What Our Learners Have To Say

Learner Support and Services

How Will upGrad Supports You

upGrad Elevate: Virtual hiring drive giving you the opportunity to interview with upGrad's 300+ hiring partners

Job Opportunities Portal: Gain exclusive access to upGrad's Job Opportunities portal which has 100+ openings from upGrad's hiring partners at any given time

FAQs on Financial Analysis Courses

1. What is a Financial Statement?

Financial Statements are the summarised data collected by the entity that shows the company’s financial condition in the given period.

2. What is Financial Analysis?

Financial Analysis is the evaluation of the financial statement of a business to understand its financial health, stability, and performance in the market. Financial Analysis plays a key role in the development of a business.

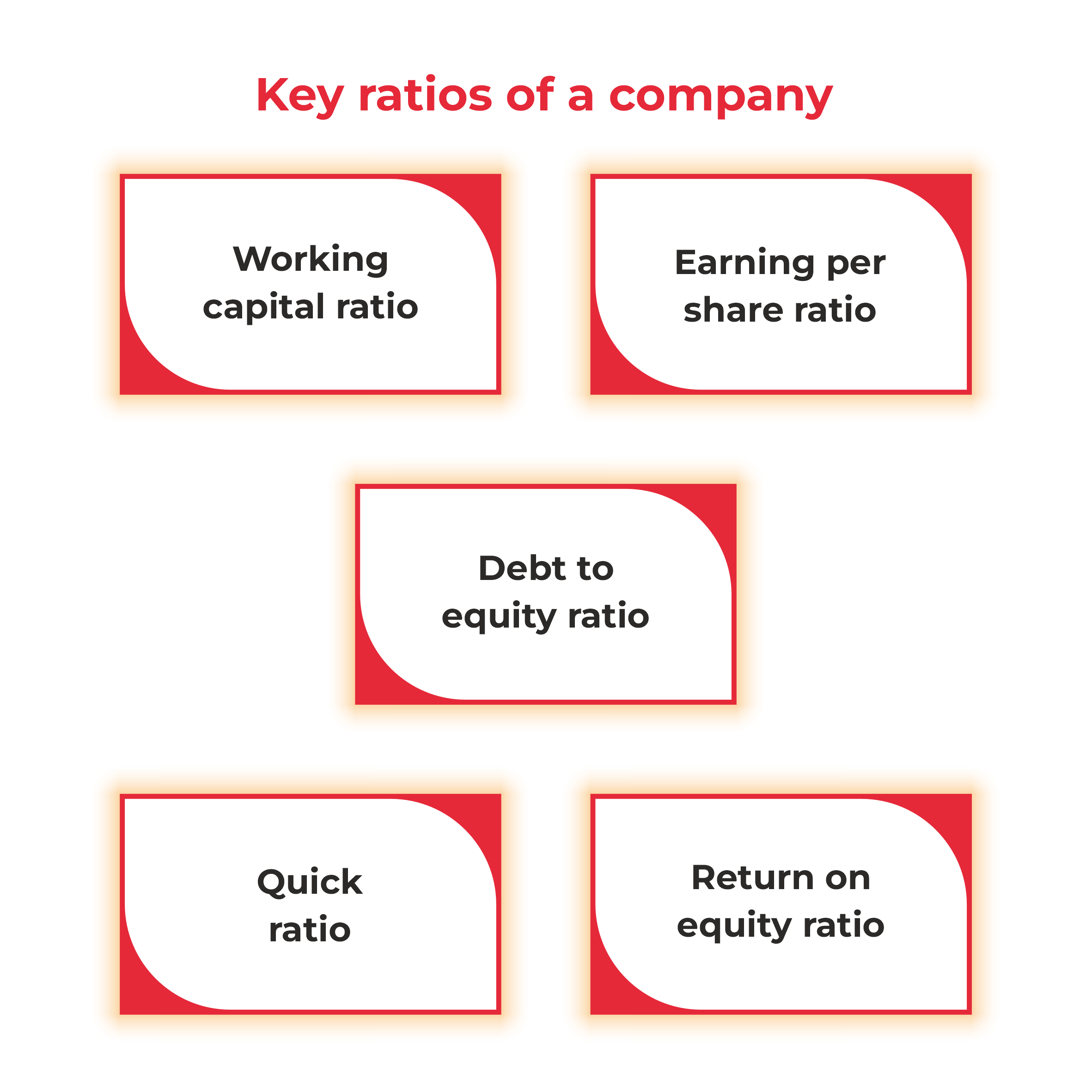

3. What are the core components of the financial statement?

The three key components of a financial statement are;

Balance Sheet

Cash Flow Statement

Profit & Loss Statement

4. Why is Financial Analysis important in any Business?

The process of financial analysis is important in a business as it gives information about its stability, solvency, liquidity, and profitability. According to the analysis, the business can further set financial policies, make strategic plans, identify projects for investment, and build long-term business plans.

5. What skills should I have to become a Financial Analyst?

There are a few skills that a person requires to become a financial analyst and to perform his task properly. Here are some of those skills;

Research skills

Analytical skills

Accounting

Auditing

Cost Optimisation

Financial Modelling and many other related skills of the field.

6. Is it a good career option to be a Financial Analyst?

Yes, it is one of the professions that is a must in any company. Without a financial analyst, the company won’t be able to understand its financial condition and take preventive measures or strategies accordingly.

7. What kind of job positions are available after learning Financial Analysis?

Once you have taken the financial analysis certification course and become a professional in the field, you have several career options. These include Finance Controller, Finance Specialist, Project Finance Manager, Specialist Financial Planning, and more. Some of the courses that help in procuring good roles in the industry include Chartered Financial Analyst (CFA), Certified Financial Planner (CFP), Chartered Public Accountant (CPA), Financial Risk Manager (FRM), and many others.

8. Typically, how long does the Financial Analysis program go?

The typical duration to complete the Financial Analysis program is 6 months to 1 year. But opting for the online course can help you get educated at your own time and pace.

9. Is Financial Analyst a good career path in India?

Yes, definitely. A professional career as a financial analyst is one of the professions that will soon escalate because of the increase in the number of businesses in India. There cannot be any successful business without a financial analyst; thus, it will always be a good career choice in India.

10. What is the average salary of a Financial Analyst?

The estimated average salary of a Financial Analyst ranges between 2.1lakh to 8.4lakh per annum.

11. How is this certification perceived by businesses?

The businesses give the financial analysis certification utmost importance and respect as the position of financial analyst is esteemed in a company.

12. Is internship an integral part after the completion of this course?

Internships are an integral part of this course because you must practice your skills on a beginner level before joining a big entity and offering them your service. Working as a financial analyst or other related fields has a crucial set of work that cannot be taken for granted, and this practice is essential.

13. Will this course help me in excelling in my career?

Of course, not only will you excel in your career, but you will also encounter a hike in your compensation after pursuing the financial analysis course.

14. How can Financial Analysts increase their salary?

To increase or promote yourself in your career graph and get a salary hike as a financial analyst, you must up your skillset. Moreover, an MBA or a master’s degree in this field can help you level up.

15. What is the highest pay for Financial Analysts?

In India, the highest pay for a financial analyst is around 10.8 lakhs per annum; abroad, the highest salary for a financial analyst is around $83,993 per annum.

16. What are the different types of Financial Analysis?

Depending on your purpose, whether you want to compare your organisation’s finance with a competitor or take an internal look at your finances, there are two types of financial analysis, Horizontal Analysis & Vertical Analysis.

17. Which are the top paying industries for a Financial Analysis Specialist in India?

- Investment Banking / Venture Capital / Private Equity - ₹11.9 Lakhs per year

- Auto Components - ₹11.0 Lakhs per year

- IT Services & Consulting - ₹9.8 Lakhs per year

- Financial Services - ₹9.3 Lakhs per year

- Consumer Electronics & Appliances - ₹6.4 Lakhs per year

upGrad Learner Support

Talk to our experts. We are available 7 days a week, 10 AM to 7 PM

Indian Nationals

Foreign Nationals